All Categories

Featured

Table of Contents

For lots of people, the most significant trouble with the limitless financial concept is that first hit to early liquidity brought on by the costs. This con of boundless financial can be lessened substantially with correct plan design, the initial years will certainly constantly be the worst years with any Whole Life policy.

That said, there are particular boundless banking life insurance plans created mostly for high very early cash money worth (HECV) of over 90% in the very first year. The lasting efficiency will certainly usually considerably delay the best-performing Infinite Banking life insurance policy plans. Having access to that additional 4 numbers in the very first few years may come with the cost of 6-figures later on.

You really obtain some considerable lasting advantages that assist you recover these very early costs and after that some. We discover that this impeded very early liquidity issue with unlimited banking is more psychological than anything else when thoroughly explored. Actually, if they definitely needed every penny of the cash missing out on from their boundless financial life insurance coverage policy in the first few years.

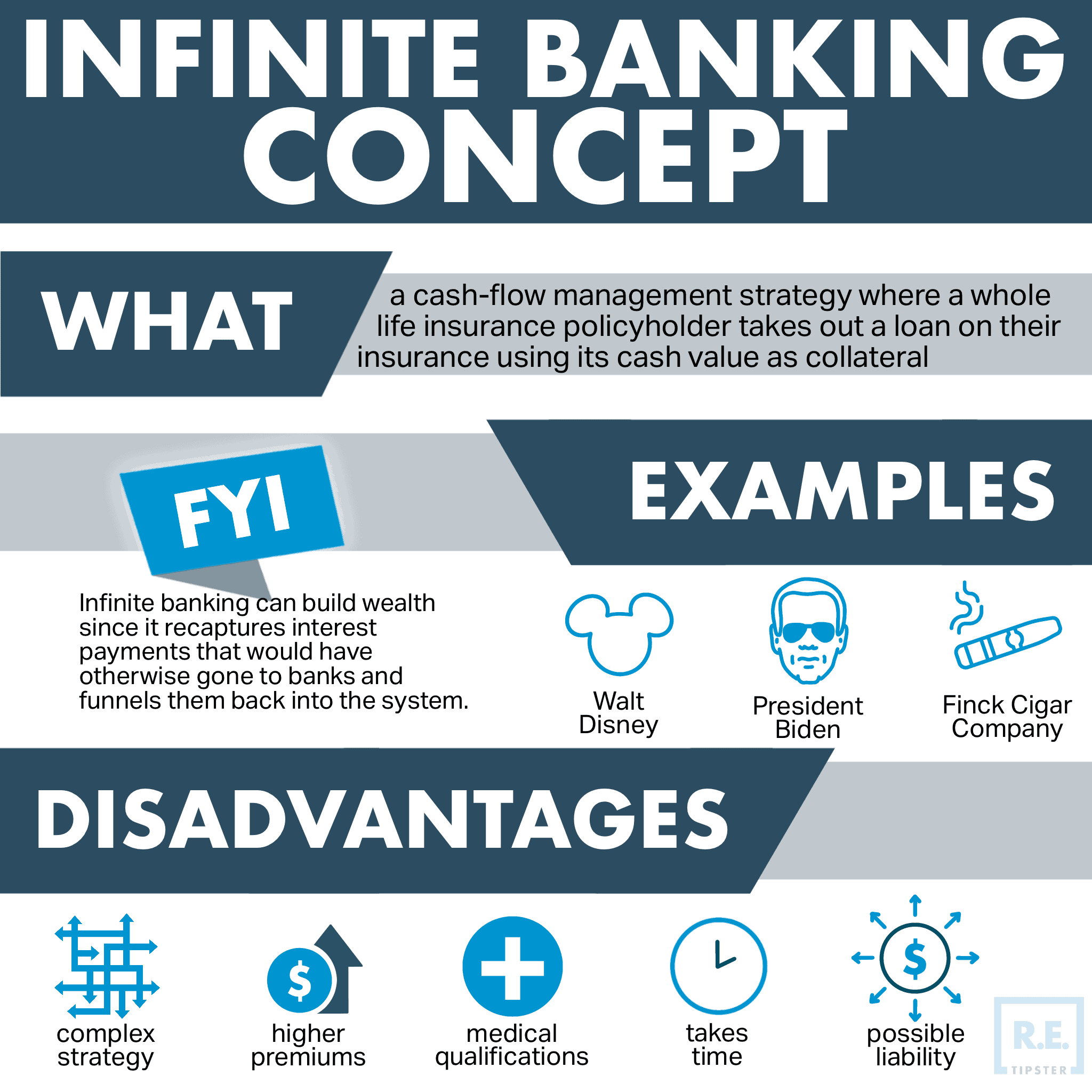

Tag: infinite financial concept In this episode, I chat about finances with Mary Jo Irmen that shows the Infinite Banking Idea. With the rise of TikTok as an information-sharing platform, monetary guidance and techniques have actually found a novel method of spreading. One such method that has been making the rounds is the limitless banking principle, or IBC for short, gathering recommendations from celebs like rap artist Waka Flocka Fire.

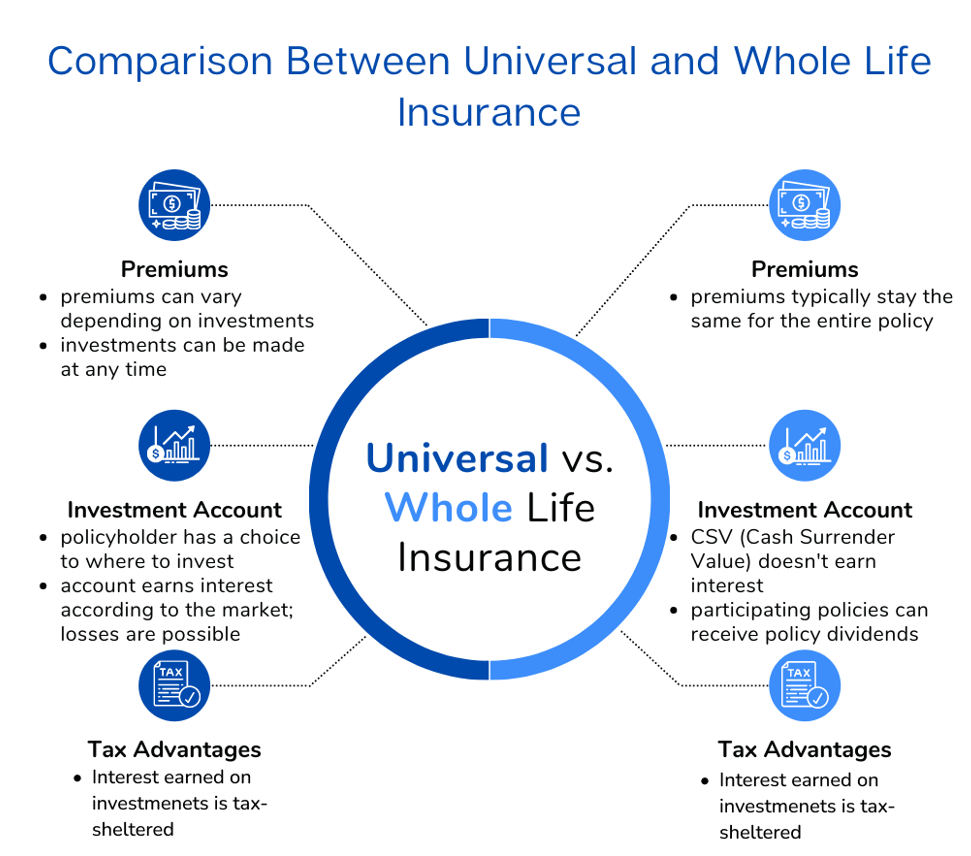

Within these policies, the cash money worth expands based upon a rate established by the insurance firm. As soon as a considerable money value builds up, policyholders can obtain a cash value financing. These loans vary from conventional ones, with life insurance coverage functioning as security, suggesting one could lose their insurance coverage if loaning excessively without ample money value to sustain the insurance policy expenses.

And while the attraction of these policies appears, there are inherent constraints and threats, demanding thorough money value monitoring. The approach's authenticity isn't black and white. For high-net-worth people or local business owner, particularly those utilizing approaches like company-owned life insurance policy (COLI), the benefits of tax breaks and compound growth could be appealing.

Infinity Banking

The appeal of infinite banking doesn't negate its obstacles: Price: The fundamental demand, a long-term life insurance policy policy, is pricier than its term counterparts. Qualification: Not everybody certifies for entire life insurance policy as a result of strenuous underwriting processes that can exclude those with details health and wellness or way of living conditions. Complexity and danger: The detailed nature of IBC, combined with its risks, may discourage lots of, specifically when less complex and less dangerous choices are readily available.

Alloting around 10% of your monthly revenue to the plan is simply not possible for many people. Using life insurance policy as an investment and liquidity source requires discipline and tracking of policy cash money worth. Consult a monetary consultant to establish if limitless banking lines up with your concerns. Component of what you review below is simply a reiteration of what has actually currently been stated over.

So before you get yourself right into a situation you're not prepared for, know the complying with first: Although the idea is commonly sold thus, you're not actually taking a lending from yourself. If that held true, you would not have to settle it. Rather, you're borrowing from the insurance coverage firm and have to repay it with passion.

Some social media sites blog posts advise utilizing money value from whole life insurance policy to pay for bank card financial debt. The idea is that when you pay off the lending with interest, the amount will certainly be returned to your investments. That's not how it functions. When you repay the finance, a part of that passion goes to the insurer.

For the first several years, you'll be paying off the compensation. This makes it very hard for your plan to build up worth throughout this time. Unless you can pay for to pay a couple of to several hundred dollars for the next decade or even more, IBC won't function for you.

Infinite Banking Simplified

Not everyone should rely entirely on themselves for monetary safety. If you need life insurance policy, below are some valuable tips to think about: Think about term life insurance policy. These plans give protection during years with significant monetary commitments, like mortgages, pupil fundings, or when caring for kids. See to it to search for the best rate.

Copyright (c) 2023, Intercom, Inc. () with Scheduled Font Style Call "Montserrat". Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Scheduled Font Style Call "Montserrat".

Infinite Wealth And Income Strategy

As a CPA specializing in actual estate investing, I've combed shoulders with the "Infinite Banking Concept" (IBC) extra times than I can count. I've even interviewed experts on the topic. The major draw, apart from the obvious life insurance policy advantages, was always the concept of developing money worth within a permanent life insurance coverage plan and loaning against it.

Sure, that makes feeling. But honestly, I always thought that cash would be better spent straight on investments instead of channeling it via a life insurance policy plan Until I discovered just how IBC can be combined with an Irrevocable Life Insurance Policy Count On (ILIT) to develop generational wealth. Let's start with the fundamentals.

Infinite Banking

When you obtain versus your plan's cash value, there's no collection settlement timetable, offering you the liberty to take care of the financing on your terms. Meanwhile, the cash money worth remains to grow based upon the plan's assurances and rewards. This arrangement permits you to gain access to liquidity without interrupting the long-lasting growth of your plan, supplied that the financing and rate of interest are taken care of intelligently.

The process proceeds with future generations. As grandchildren are born and grow up, the ILIT can buy life insurance policy plans on their lives. The depend on after that gathers numerous plans, each with growing cash money values and survivor benefit. With these plans in position, the ILIT properly ends up being a "Household Bank." Relative can take financings from the ILIT, making use of the money worth of the policies to fund investments, begin businesses, or cover significant costs.

An important facet of handling this Household Bank is the use of the HEMS requirement, which represents "Wellness, Education, Maintenance, or Assistance." This standard is usually consisted of in trust arrangements to route the trustee on how they can disperse funds to recipients. By adhering to the HEMS requirement, the count on ensures that distributions are produced vital demands and lasting assistance, safeguarding the count on's possessions while still attending to member of the family.

Increased Versatility: Unlike rigid small business loan, you regulate the settlement terms when borrowing from your own plan. This enables you to framework payments in such a way that straightens with your company cash flow. infinite bank. Improved Capital: By financing overhead with policy finances, you can possibly liberate cash money that would certainly or else be locked up in conventional car loan payments or devices leases

He has the exact same equipment, yet has likewise developed added money value in his policy and got tax obligation benefits. Plus, he now has $50,000 readily available in his policy to use for future opportunities or expenditures. Regardless of its potential benefits, some people remain doubtful of the Infinite Banking Idea. Let's resolve a few common problems: "Isn't this simply costly life insurance policy?" While it holds true that the premiums for a correctly structured entire life plan might be more than term insurance coverage, it is very important to view it as greater than just life insurance coverage.

Infinite Banking Uk

It has to do with creating an adaptable financing system that offers you control and provides numerous benefits. When used strategically, it can enhance other financial investments and service approaches. If you're intrigued by the potential of the Infinite Banking Concept for your organization, here are some steps to take into consideration: Inform Yourself: Dive deeper into the concept with reputable publications, seminars, or appointments with knowledgeable experts.

{kind=link}

Table of Contents

Latest Posts

A Life Infinite

Dave Ramsey Infinite Banking Concept

Private Banking Concepts

More

Latest Posts

A Life Infinite

Dave Ramsey Infinite Banking Concept

Private Banking Concepts